As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

While roughly 1 in 10 Americans faces food insecurity, rural communities are particularly affected. Rural communities comprise 63% of all U.S counties but 87% of the counties with the highest rates of food insecurity.

The challenge facing rural consumers is largely born of a lack of access, with literally dozens of U.S. counties lacking food stores. In addition, only 37% of rural residents have access to major food delivery services.

Convenience stores, dollar stores and other retailers have worked to pick up the slack in rural areas, but run into the same issue as supermarkets: a lack of a sizable consumer base.

Co-ops and similar retail concepts have kept grocery stores operating in some rural communities, though these are generally found in towns and counties with a concentration of residents.

Technological innovation in the areas of driverless and drone delivery could ultimately ease access and potentially even provide food/beverage brands with a more direct relationship with their consumers.

Low income: a poverty rate of 20% or greater, or a median family income at or below 80% of the statewide or metropolitan area median family income

Low access: at least 500 persons and/or 33% of the population living more than one mile from a supermarket/grocery store (10 miles in the case of rural census tracts)

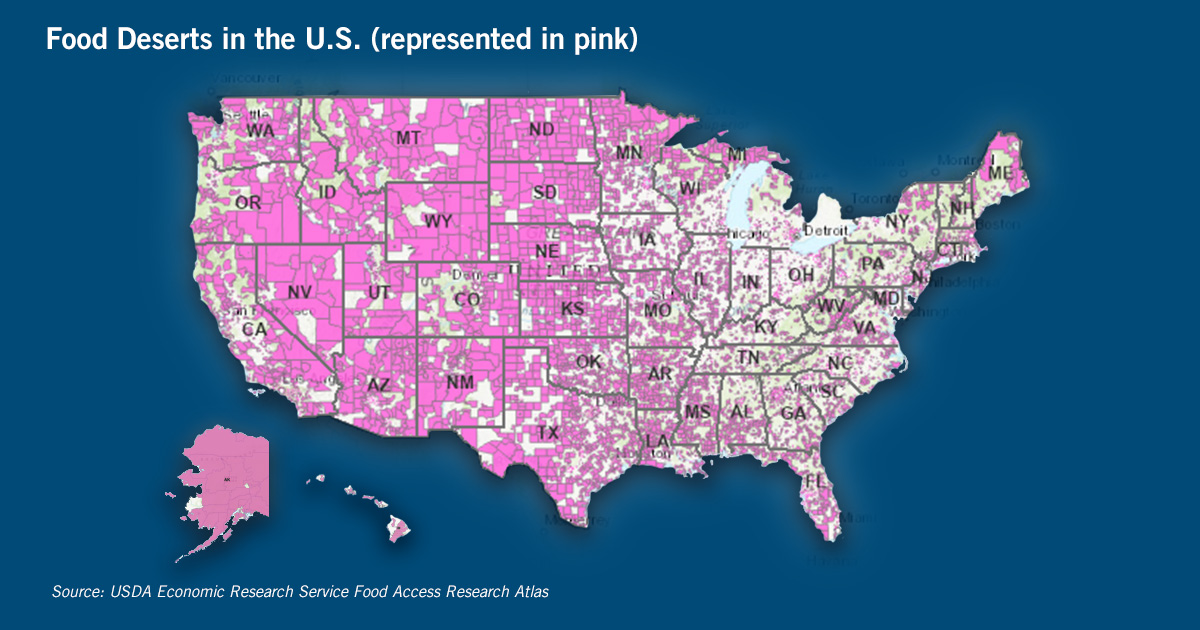

This report focuses on low-access food deserts, where the distance impedes the ability for households to reach food stores.

Access to food stores

The USDA has good reason define food deserts in two different ways. As the agency noted in its Low-Income and Low-Foodstore-Access Census Tracts, 2015-19 report, people with low incomes actually lived closer to food stores than those with moderate and high income. Households participating in the Supplemental Nutrition Assistance Program (SNAP) were more likely than non-SNAP-participating households to live within 0.5 miles of the nearest food store and less likely to be more than 1 mile from the nearest store. The report also noted proximity to food stores improved over that five-year span, largely the result of an overall increase.

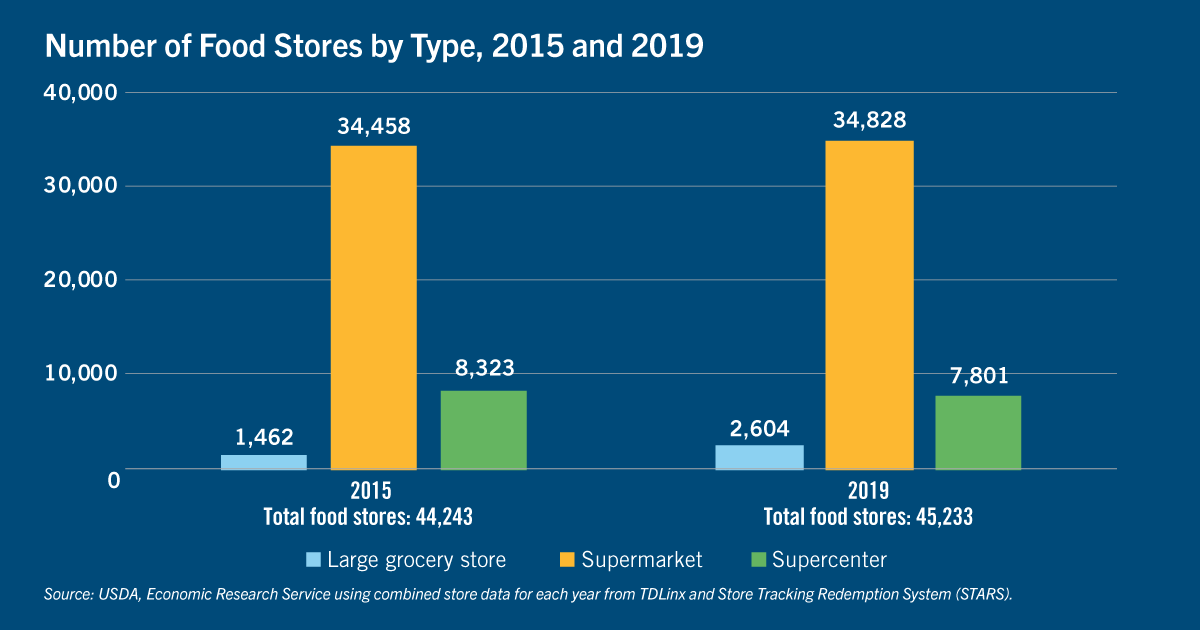

Here, the USDA's definition of supermarkets and large grocery stores includes food stores with at least $2 million in annual sales and containing all the major food departments. Nevertheless, food deserts cover a sizable portion of the country.

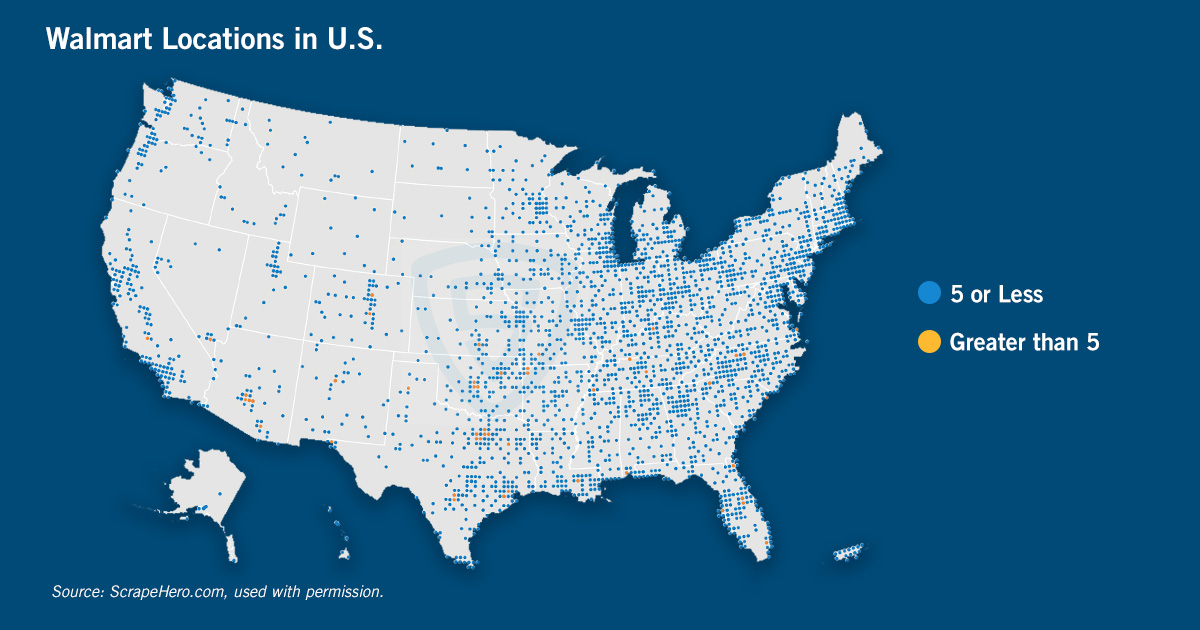

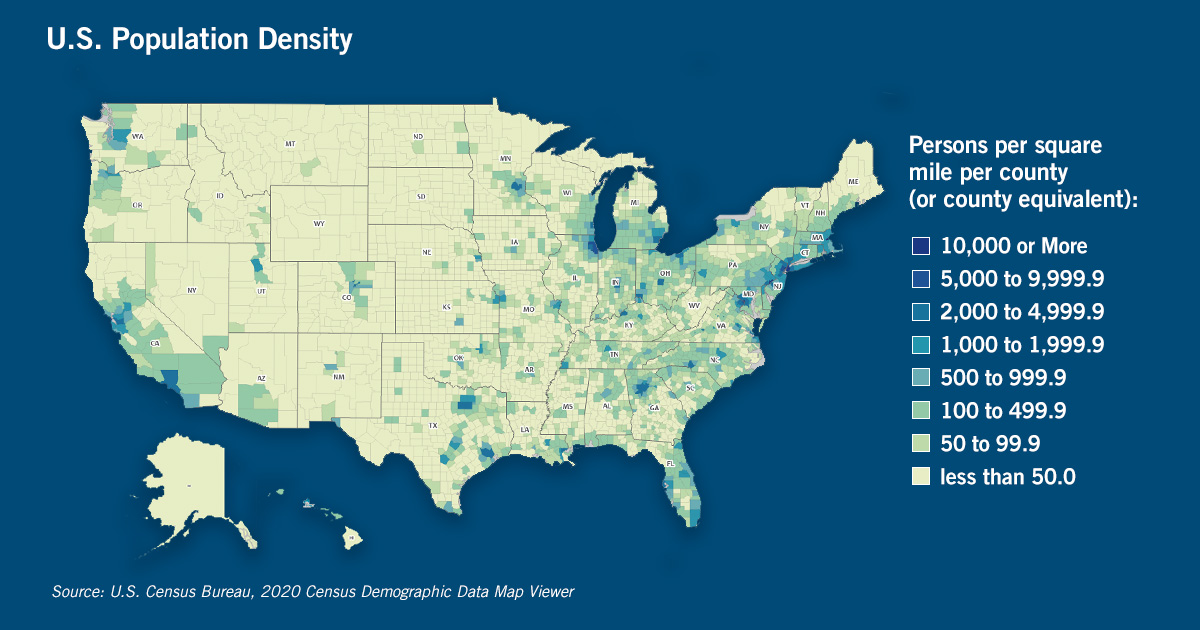

Clearly, food stores follow population. Walmart is the largest food retailer in the U.S. but its stores are unevenly distributed among states, much less counties. Texas has 601 Walmart stores, while North Dakota has 17 and Wyoming has 14. Walmart’s locations are a good indicator of overall population density, with a large presence in the East and South, and thinner in the West (aside from the West Coast and isolated metropolitan/suburban areas). The geographic gaps where the nation’s largest food retailer has not penetrated are considerable. Granted, the population of these areas may be too sparse to support a Walmart store.

Such a perception furthers the food-scarcity issue and could reflect where ecommerce (whether from Walmart, Amazon, Instacart, even potentially direct-to-consumer efforts) could be a solution.

Delivering directly to consumers

Food delivery has become an expected service for many Americans. The Brookings Institution finds 93% of the U.S. population (including 90% of people living in food deserts) has access to food delivery from at least one of four major players: Amazon (Fresh or Whole Foods Market), Instacart, Uber Eats or Walmart. But for limited-access food deserts, the issue remains the same: The Brookings Institution found delivery zones are concentrated in larger metropolitan areas, with only 37% of rural residents having access to any of the analyzed food delivery services. Barriers are not just the lack of sufficient broadband access or service (either fixed or mobile), but also a lack of awareness or comfort with shopping online. Delivery mechanisms themselves present a considerable challenge, as well.

Nevertheless, agribusinesses and food manufacturers looking to establish a more-direct line to their consumers may consider adopting tactics seen during the height of the pandemic. Farmers in rural America expanded their own delivery capabilities to meet consumer demand that stemmed from consumers’ efforts to isolate at home, as well as a solution for empty grocery store shelves. Reuters at the time noted farmers were delivering to homes in areas where grocery delivery from the likes of Instacart and AmazonFresh were not widely available.

Store alternatives to supermarkets

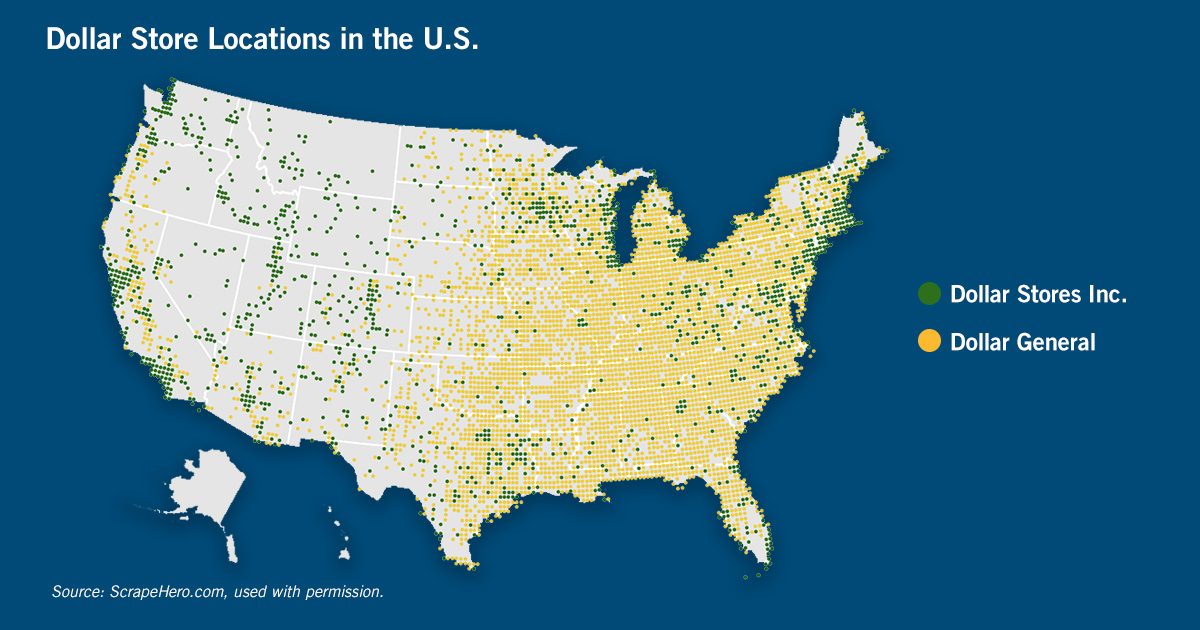

Convenience stores, dollar stores and even liquor stores have been suggested as possibilities for reducing food insecurity in more rural areas. For liquor stores in particular, delving into food (particularly fresh produce) brings considerable challenges for distribution and store management logistics and labor. The even greater challenge may be navigating as a retailer oriented to adult consumers to offer fresh foods for all ages.

Convenience stores and dollar stores, however, have focused increasingly on foods, though the latter are finding margins in that space elusive. Dollar Tree, for example, recently pared down its fiscal year profit expectations, the result of "an increase in low-margin purchases such as food," as well as issues with shrink and fuel costs. Dollar General, meanwhile, is implementing a "food first initiative" that puts it much more in competition with both convenience stores and traditional grocers. In fact, Dollar General is building a distribution center in Arkansas that will help more of its stores sell fresh produce. Regardless, the issue with dollar stores is much the same as with those traditional grocers: Their locations are driven by population density.

Retaining local grocery options is important for the survival of rural communities. CoBank and Food Co-op Initiative (FCI) have worked together over the past five years to expand programs for rural communities that have lost (or who are at risk of losing) local grocery options. Such local grocers face challenging competition but, at the same time, can appeal with local products and offerings tailored to community-specific needs. An example is Marmaton Market in Moran, Kansas. A for-profit corporation operating under cooperative principles proved to be the solution for the town of 500. Now looking to bring more locally produced goods into the store, the store emphasizes local as a means of supporting the economy, building morale and creating a stronger sense of community.

A similar approach helped save Royal Super Mart in Sheffield, Illinois, a village of approximately 800, and kept the rural town from joining the statistics of counties that have seen a decline in grocery stores. As of 2015 (the most recent data available from USDA ERS), 44 U.S. counties have no grocery stores; 40 of them were rural. A June 2021 report from ERS found the median number of grocery stores per capita decreased by 40% for rural and urban nonmetro counties from 1990-2015, with a particularly acute drop after the Great Recession. Less access to grocery stores has, in turn, led consumers in these areas to purchase food at convenience stores, the report attests. The authors opted against evaluating the impact this change has had upon food access, as well as the overall challenges for consumers living in even more rural areas.

Moving beyond brick and mortar

Regardless, with 10% of the country experiencing some degree of food insecurity, the market is there. The question, particularly among those in rural communities, is how to foster access to food and beverages. Food insecurity in America takes many forms, and means to address the issue must be diverse. Meeting the food needs of rural America will not necessarily mirror those that can address food insecurity in urban areas. Yet, particularly for shelf-stable food and beverage, delivery mechanisms exist, even if it takes the form of FedEx, UPS or USPS. Fresh food offerings present another challenge altogether, but more direct-to-consumer approaches should, in the long term, be able to capitalize on improvements in technology (whether drone delivery or driverless trucks) to reach those who simply don't live near a grocery store.

Futuristic delivery and supply chain innovations appear to be taking root at several large, brand-name companies. In collaboration with Gatik, Tyson Foods will deploy AI-assisted autonomous trucks to haul prepared meats over predetermined short-haul routes to distribution and storage facilities in northwest Arkansas. Tyson identified these routes as well-suited for autonomous operation, as they are highly repeatable and generally within state lines (simplifying any regulatory issues). Admittedly, northwest Arkansas is far from being a food desert, but such automated processes and delivery mechanisms could bridge the gap for consumers with limited access to food stores.

These examples are indicative of where retailers — whether grocery stores or even convenience stores or dollar stores — could serve rural consumers and offset the issue of food insecurity stemming from limited access. In addition, food/beverage manufacturers themselves could incorporate such technologies for more of a direct-to-consumer relationship and establish their respective brands as part of the consumer’s ensconced ordering procedures.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.