As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

U.S. new-crop soybean export sales will start the upcoming 2024/25 marketing year at a historically slow rate as international buyers remain discouraged by a strong U.S. dollar, slowing economic growth, and uncertainty over U.S. trade policy in an election year.

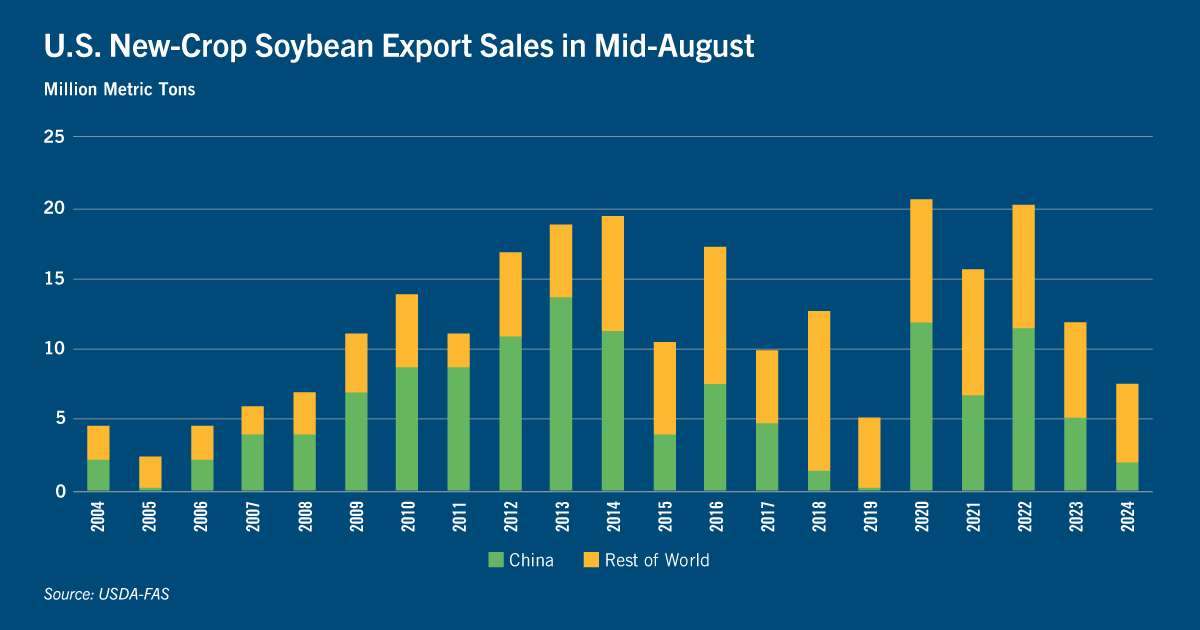

China typically accounts for most U.S. soybean export sales. However, Chinese bookings of new-crop U.S. soybeans are the slowest in nearly two decades – aside from the low achieved during the trade war in 2019 – despite a resurfacing of new purchases in recent weeks.

China is not alone in its reluctance to buy U.S. soybeans. Accumulated new-crop U.S. export sales to other countries are also historically low.

The slow start to the export season, though, does not necessarily mean a bad year ahead. The pace of early season bookings historically has a low correlation with final export numbers for the marketing year.

A smaller-than-expected South American harvest, a bump in European demand for soybeans from non-deforested acreage, lower interest rates in the U.S., and a recovery of the Chinese economy could rejuvenate export demand for U.S. soybeans in the marketing year ahead.

The U.S. is entering the 2024/25 soybean marketing year, which starts Sept. 1, with an abysmal export sales pace for new-crop bookings. As of mid-August, new-crop U.S. export sales to all destinations were the lowest since 2008 for the same period – aside from the low achieved in 2019 during the trade war with China. A strong U.S. dollar, ample South American harvests, a slowing global economy, and trade policy uncertainty in an election year in the U.S., have hobbled the U.S. export pace heading into an anticipated record soybean harvest. September to December is the peak shipping period for U.S. soybeans with typically more than half of all shipments for the season occurring in those four months before the arrival of the South American harvest.

While Chinese demand for U.S. soybeans has recently resurfaced, sales are still lagging far behind prior years. China, which typically accounts for over 60% of world soybean imports and more than half of all U.S. soybean exports, currently has the second-lowest volume of purchases for new-crop U.S. soybeans in 20 years.

Chinese demand for U.S. soybeans this fall remains in question following China’s aggressive purchases of Brazilian soybeans this year. China’s purchases of Brazilian soybeans surged to a record pace in 2024 as Chinese buyers took advantage of low Brazilian prices and a weakening Brazilian currency. U.S. export sales to other destinations, though, are also historically low.

The U.S. soybean export program faces a number of obstacles in the weeks and months ahead, particularly with Chinese demand. China’s economy grew at a meager 4.2% last quarter as China grapples with a struggling real estate sector, rising debt and weak consumer spending on food. China’s economic slowdown is dragging meat demand and causing hog breeders to shrink sow herd sizes.

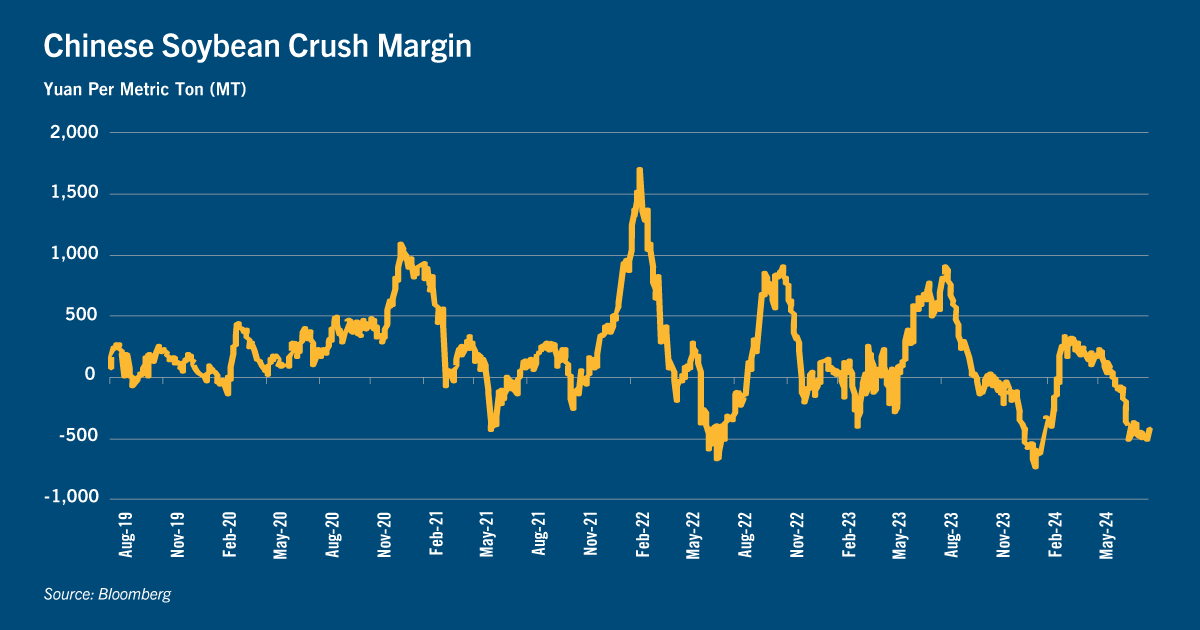

Chinese crush margins are now historically low on the heels of record soybean imports from Brazil and slowing feed demand. At the Dalian Commodity Exchange, soybean meal prices have fallen 19% in the last three months, soybean oil prices are down 8%, and soybean prices are down 4%. Chinese soybean crushers have suffered negative crush margins this summer with margins falling to the lowest level in 18 months. As China’s hog herd atrophies and feed demand slows, crushers will likely slow their purchases for the remainder of 2024 to digest the growing stockpile. La Niña events also tend to have net positive effect on crop productivity in China, which could further dampen demand for soybean imports.

Does a slow start to the export season mean a poor finish?

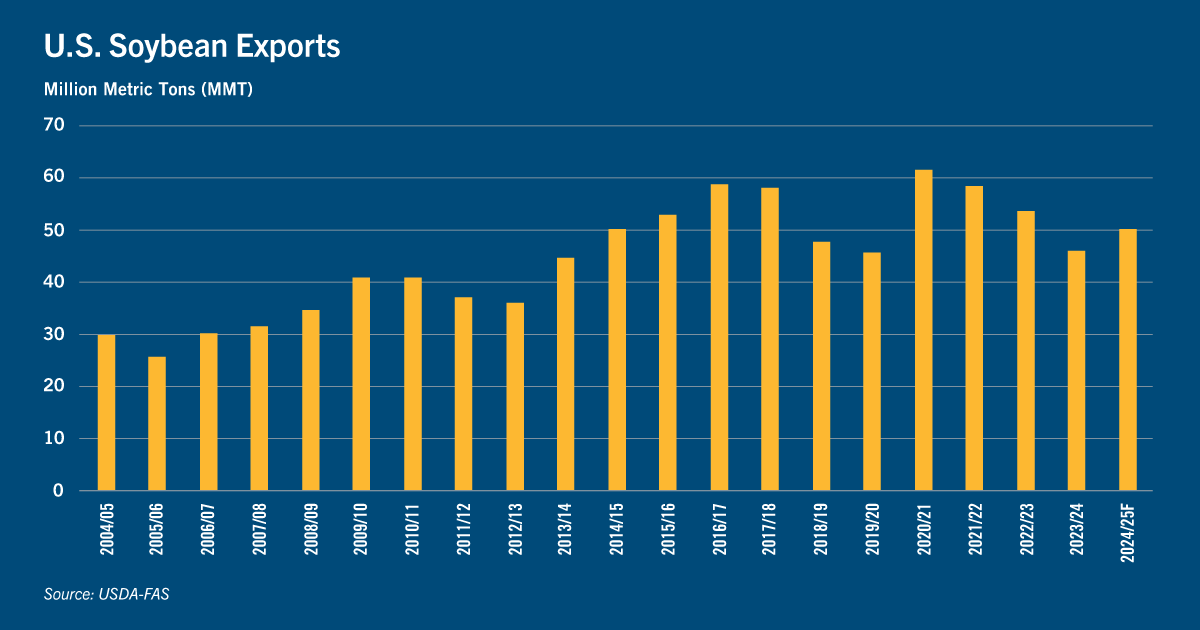

A slow start to the export sales pace, though, does not guarantee a bad year ahead for U.S. soybean exports. Over the past 20 years, the export sales total for new crop soybeans at the end of August has been a poor indicator for total soybean shipments by the end of the marketing year.

Despite the poor start to the season, U.S. soybean exports could benefit from a multitude of tailwinds. U.S. soybean prices have already fallen to the lowest level in four years. With a record U.S. soybean harvest expected this fall, increased availability and continued weakness in prices will attract new export demand.

The size of the South American harvest will also impact the volume of U.S. export business. USDA currently forecasts a record Brazilian crop of 169.0 million metric tons, up 10.5% YoY. Private forecasts have put the Brazilian harvest above 170 MMT. However, low prices may discourage Brazilian farmers from expanding soybean acreage as planting commences in the coming weeks.

La Niña may also negatively impact Brazilian crop yields. The National Oceanic and Atmospheric Administration currently forecasts La Niña to emerge September to November. In 2021/22, La Niña caused drought conditions throughout much of Brazil’s key soybean-growing regions, particularly in the south. The drought resulted in a 6.5% YoY drop in soybean production. A material drop in the Brazilian harvest will divert some export business back to the U.S.

New European demand for U.S. soybean is expected to emerge after the new year. In May 2023, the European Commission adopted the Deforestation-free Supply Chain Regulation (EUDR), which targets products identified as drivers of deforestation, including soybean and palm derivatives. Starting Dec. 30, 2024, European products sourced from standard- or high-risk origins must comply with additional risk assessment and mitigation procedures. Imports must be certified to not have come from land deforested in the past decade, giving an advantage to U.S. soybeans over South American soybeans into the EU market. The EU typically imports 13 MMT to 15 MMTs of soybeans annually.

A recovery in China’s economy may lift Chinese crush margins, causing crushers to work through stockpiles at a faster rate and continue with soybean purchases. China's central bank, The People's Bank of China (PBOC), unexpectedly cut interest rates in June amid the worsening economic outlook, with more rate cuts widely expected. With the PBOC stimulating the Chinese economy through lower rates, the boost could raise consumer demand for meat and lift demand for soybeans and soybean meal.

Future interest rate cuts from The Federal Reserve may also drive money back into emerging markets like Brazil, strengthening Brazil’s currency against the U.S. dollar. A stronger Brazilian real versus the U.S. dollar will give U.S. soybeans an advantage in the export market.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.