As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

Protein’s strong consumer following is fueling producer optimism.

A favorable feeding environment typically spurs herd expansion, yet the outlook for livestock herd and poultry flock growth remains moderate overall.

The trade front remains complicated. With strong global demand and new barriers to trade, including disease, the market is subject to heightened volatility.

Protein is everywhere. Is it a flailing fad or a growing trend? Cargill’s 2025 Protein Profile study showed 61% of consumers reported an increase in protein consumption in 2024 compared with 48% in 2019.

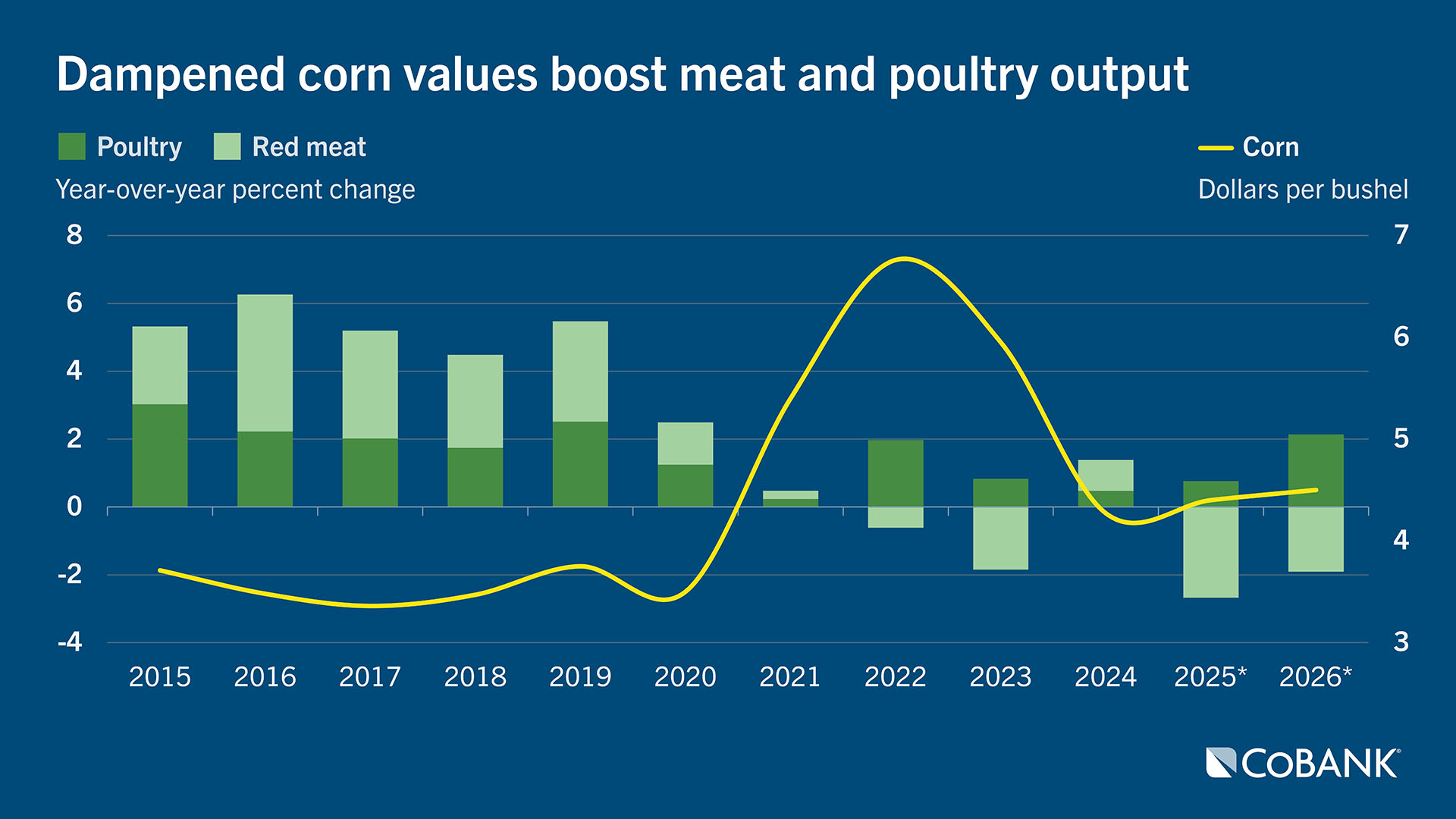

Despite rising price points for meat and poultry and expanding protein-centric competition, animal protein demand remained strong throughout 2025. Exceptional demand and softening feed prices are encouraging expansion in the animal protein space. At the farm level, the combination of boosted revenues and depressed corn and soybean prices offers optimism in the year ahead but not to the degree that expansion is expected to proliferate.

Source: LMIC, USDA

*LMIC 2025 estimate/2026 forecast for meat and poultry; CoBank 2026 forecast for corn

Historically, when corn prices are high, livestock meat production pulls back. However, as commodity crop prices fall, animals will stay on feed longer or have access to higher quality feedstuffs to gain more weight per pound of feed. For 2026, USDA forecasts poultry production will grow by 2.1% year-over-year, the largest change since 2019. As cattle availability declines next year, beef output is forecast down 4.7%, further dampening red meat production.

Livestock supply conditions have grown notably tighter in the last two years and are likely to remain so over the next 12 to 18 months. As a result, feeding efficiencies—doing more with less—remain paramount, and we expect that to be a prominent feature in 2026.

Source: LMIC, USDA, CoBank calculations

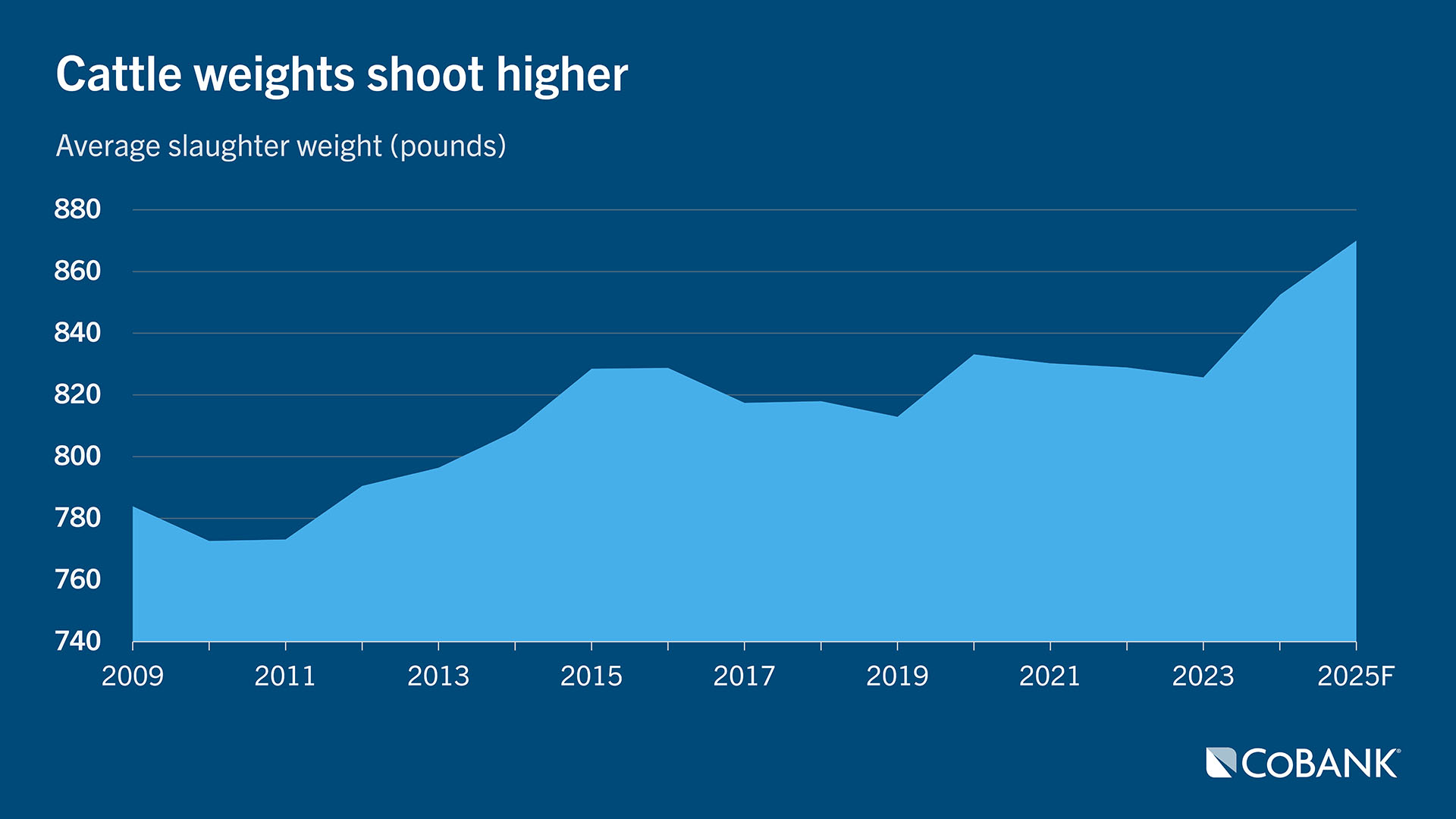

After rising just 4 pounds annually over the last 20 years, cattle weights spiked by 27 pounds in 2024 and another 24 pounds, or 2.5%, through September 2025, averaging more than 870 pounds per head. The modern steer carcass is 130 pounds heavier than the 2005 version. We question how much higher weights can go without affecting high-end cuts like the ribeye.

Source: USDA, LMIC

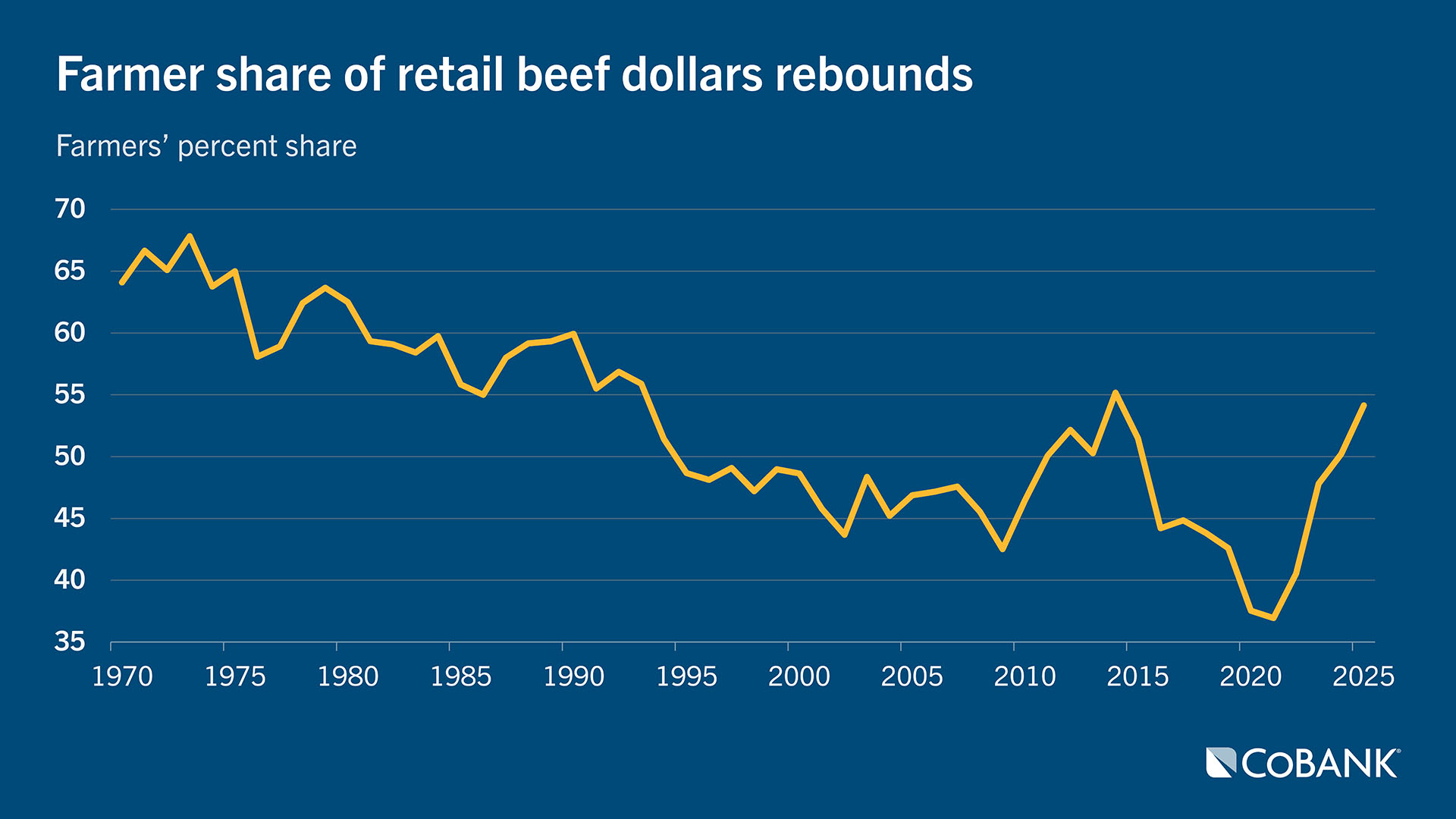

Supply constraints coupled with booming beef demand resulted in record-high retail beef prices in 2025. Elevated cattle prices have shifted more of the retail beef dollar share to producers. Through August 2025, producers received $0.54 of every retail beef dollar spent, the highest since 2014 and the peak of the last cattle cycle. We attribute this gain to the consumer recognizing the access they have to high-quality beef. Exceptional quality should push beef prices higher in 2026.

Chicken is another bright spot in the protein sector. With annual consumption now averaging well over 100 pounds per person, chicken consumption is the fastest growing of any meat. Chicken won big with the food flavor and concept explorers at quick-service restaurants and fast casual dining in 2025. Spot market breast meat prices were about 25% below year-ago levels to end 2025, encouraging chicken featuring and innovation.

Although this optimism in protein is strong, several severe headwinds could hinder the animal protein sector in the coming year. New and recurring diseases have popped up and spread throughout livestock in the U.S. including highly pathogenic avian influenza, New World screwworm, avian metapneumovirus, and porcine reproductive and respiratory syndrome, to name a few. Trade restrictions and barriers could prove futile as the U.S. exports variety and offal meats that have a stronger demand market in other countries. Finally, labor remains a challenge both on farm and in processing facilities, which is accelerating investment in technology and equipment.

Falling feed costs amid strong demand and expansion constraints promote optimism for animal protein space. We expect growing desire for protein inclusion will surpass “fad status” in the upcoming years and transform Americans’ purchasing behavior for years to come.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.