As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

Restaurants face continued foot traffic erosion as rising prices pressure consumers.

Value-focused offerings proliferating on restaurant menus could become white noise with little distinguishing them from peers.

Retail food and beverage face not only cost-sensitive consumers but also a quasi-regulatory demand for less-processed options without artificial ingredients.

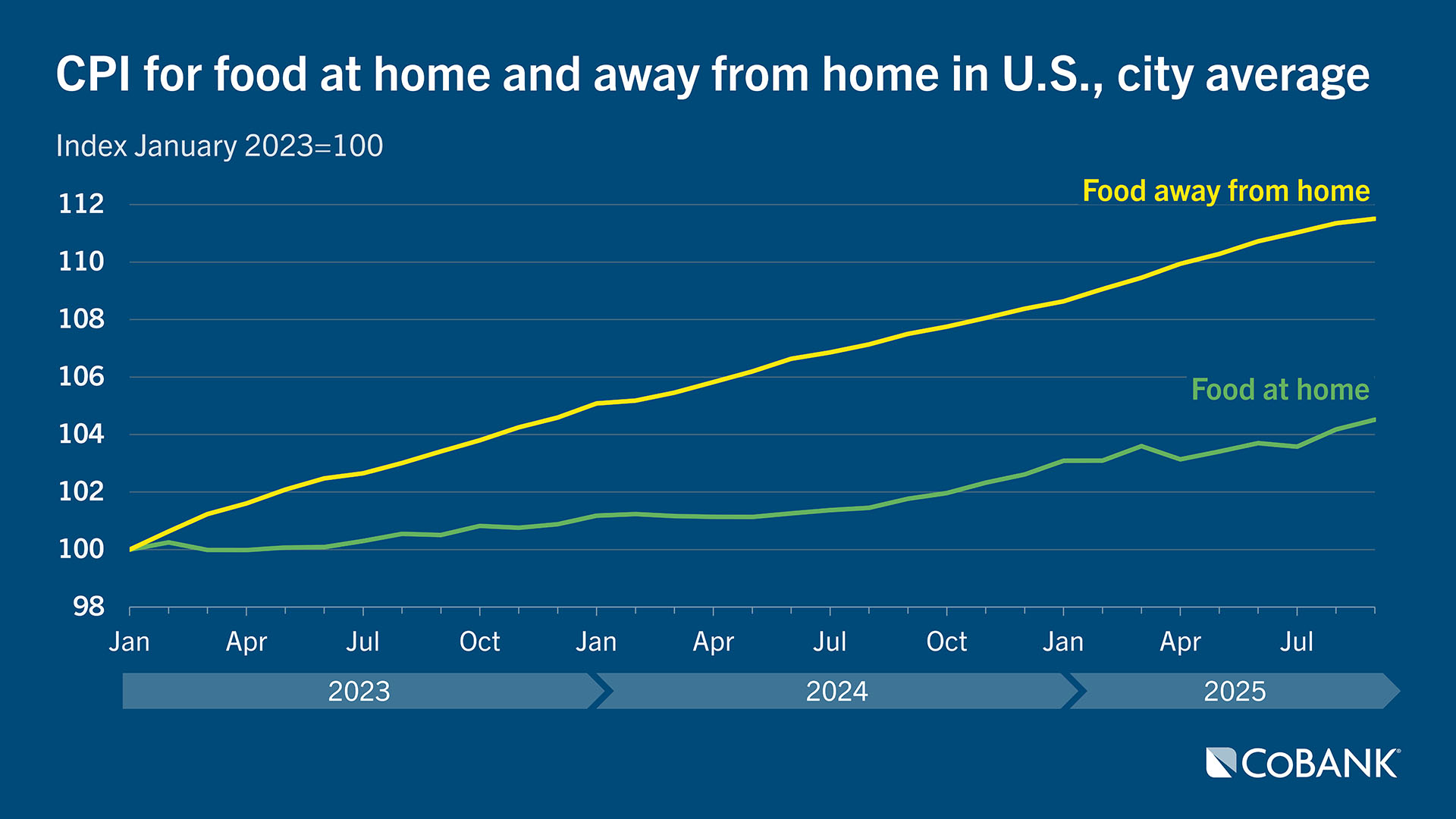

Restaurants are showing further signs of weakness as higher prices are taking a toll on consumer dining-out behavior, and little indicates a shift soon. Year over year, menu prices jumped 3.7% in September, well below the 8.8% peak in March 2023 but still considerable growth. And with restaurant prices still rising faster than food-at-home costs, consumers continue to shift food consumption to at-home—a trend showing no signs of stopping.

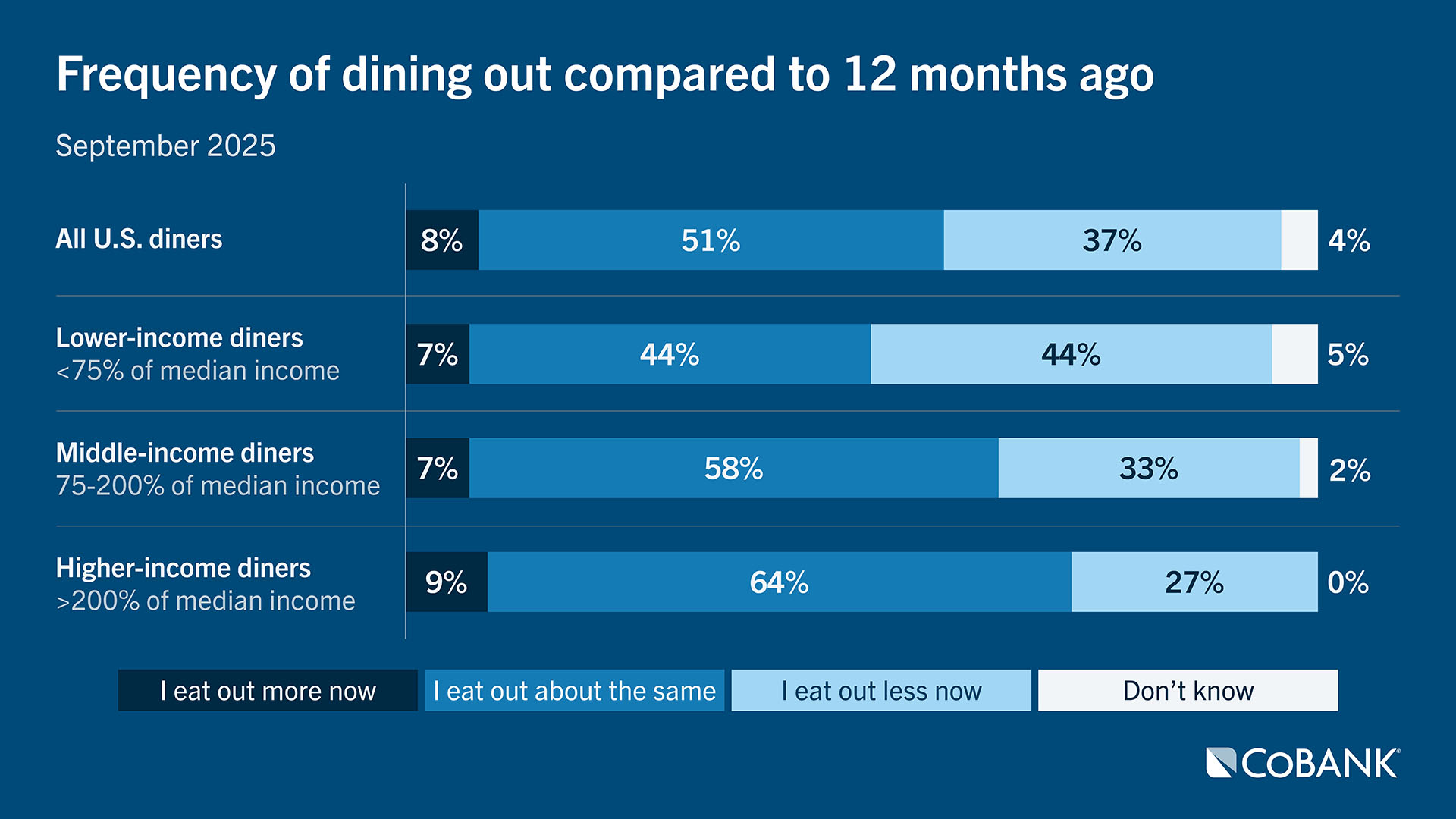

Source: YouGov U.S. dining out report 2025

According to YouGov’s 2025 U.S. Dining Out Report, 37% of Americans are dining out less frequently over the past 12 months, including 44% of lower-income consumers. Nearly 7 in 10 (69%) are dining out less specifically because of restaurant price increases. Among diners cutting costs, 60% are choosing cheaper restaurants, while 53% are using discounts or coupons; however, those tactics are finding their limits.

Even restaurants that fared relatively well up until now have begun to underperform. Chipotle Mexican Grill in October cut its fiscal year outlook for the third time this year, citing challenges from consumers in their 20s and 30s—the very demographic that had helped propel the fast-casual restaurant segment. Shake Shack cited similar data and “pressure on lower-income consumers” in its own earnings call. Indeed, the only fast-casual chain not to issue warnings of late, Chili’s, has seen foot traffic continue to grow (+13% in the most recent quarter, when same-store sales grew by double digits for the sixth straight quarter).

Chili’s will be hard-pressed to continue that run, however. As of next quarter, Chili’s year-ago performance was 20%-plus, and the chain is tempering expectations by noting same-store sales will hover in the mid-single-digit range for the balance of the fiscal year. Unmentioned in Chili’s call was the increased emphasis on value deals from other fast-casual chains, a group including Denny’s, Applebee’s and IHOP, all of which are leveraging value menus that put them in direct competition with the quick service restaurant segment—and that they hope will resonate with younger and lower-income demographics who have slowly turned away from restaurants.

The fallout from these challenges among restaurants has begun to emerge and will likely take further shape in the year ahead as restaurant brands streamline their operations and offload underperforming concepts. The first shoes to drop were among pizza chains. Historically a cost-effective meal solution, a pair of major pizza chains are struggling not only with consumer sales but in finding buyers. Papa Johns is on the market and was set to go to Apollo Global Management, until the firm withdrew its $2.1 billion offer in October. This comes as Yum Brands is positioning Pizza Hut for a sale. The one-time pizza giant remains a huge entity—the second-largest pizza chain in the country—but has endured seven straight quarters of same-store sales declines. Yum stablemate KFC has hardly fared better but is likely safe from divestment due to its success with its tenders-focused concept, Saucy. KFC is also a key player in the country’s continued trend toward chicken, a relatively cost-effective protein whose inflation-related increases have been notably less than other animal proteins.

Cumulative price increases weigh on consumer behavior

Inflation rates paint only a part of the story for most consumers, however. Price increases are tolerable to a point, but the challenge for many brands— and for foods and beverages in general—has been the cumulative effect of these price increases in recent years. Consumers simply are balking at paying 15% more for a hamburger or 20% more for a cup of coffee than they were just four or five years ago.

Source: U.S. Bureau of Labor Statistics

At the same time, retail grocery brands face not only increasing input costs but also a push to reduce artificial ingredients. Most concerning for those brands must be that the impetus for these reductions is not entirely based on consumer wishes. Announcing Simply NKD versions of Cheetos and Doritos, PepsiCo Foods U.S. CEO Rachel Ferdinando noted, “It wasn’t based on consumer data or trends. No insight would ever suggest removing color from Doritos or Cheetos, because these are fan favorites.”

Ferdinando’s comments suggest a troubling future for consumer packaged goods food and beverage brands in the coming year. Significant regulator encouragement to reduce artificial ingredients comes with considerable costs associated with switching formulations of established (and popular) brands to incorporate natural elements. This is all with little data either in terms of surveys or behavioral trends indicating that consumers actually want—much less will pay more for—these reformulated products.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.