As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

Global grain and oilseed markets are experiencing oversupply, but optimism is rising due to increased biofuel production and improved export conditions.

Record harvests in South America are reducing U.S. competitiveness in oilseed exports.

Demand for U.S. grains and oilseeds is expected to strengthen as lower prices stimulate usage.

Global grain and oilseed markets remain oversupplied, but increased biofuels production and improving export conditions are boosting U.S. producer optimism that prices have passed their cyclical bottoms.

After a year of trade uncertainty between the U.S. and China, a partial détente in the trade war has resulted in a quick flurry of soybean sales to China, but current price dynamics—Brazilian origin is likely to remain the significantly cheaper option in coming months—suggest that a return to historic U.S. export volumes is unlikely.

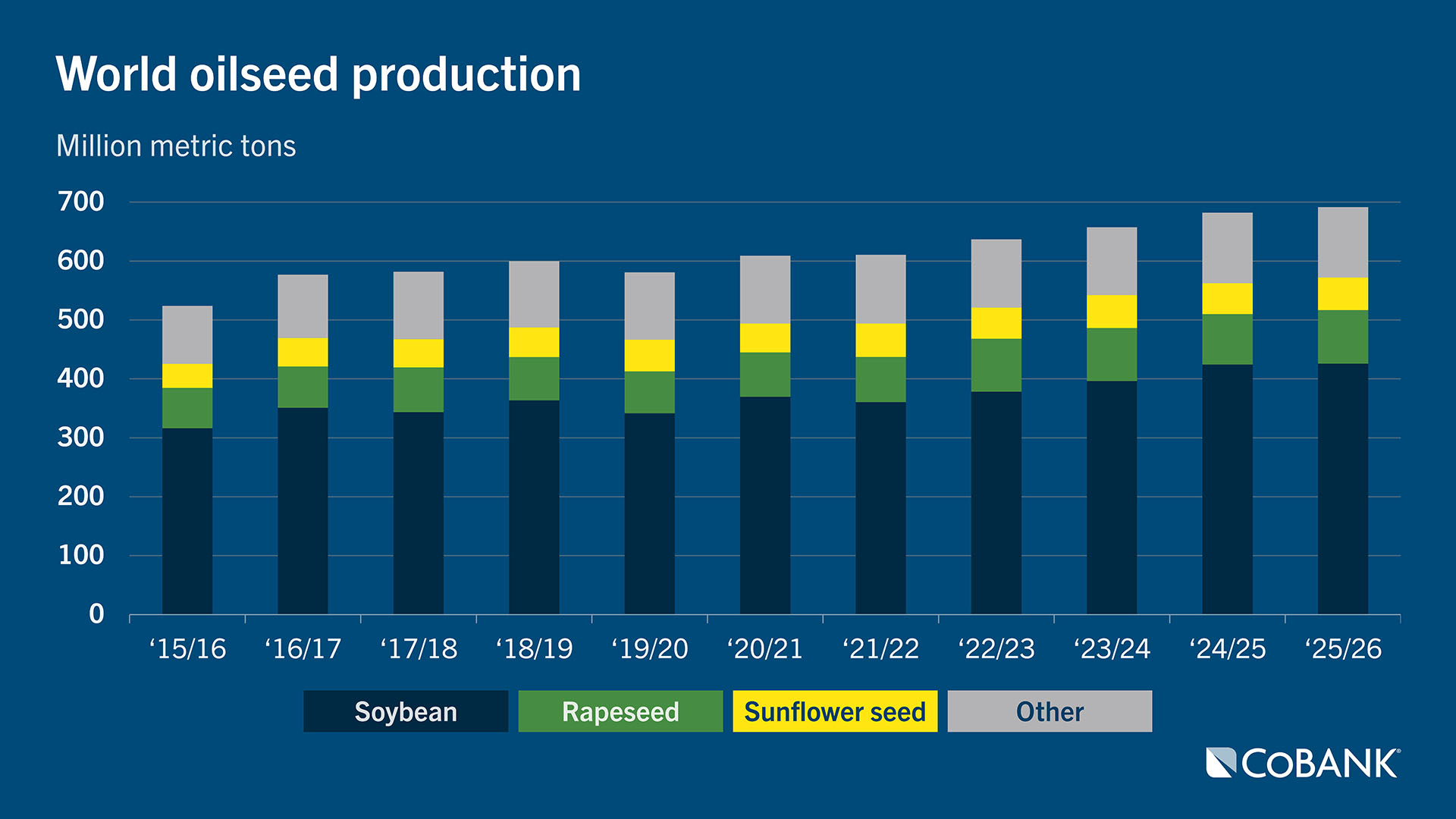

Source: USDA-FAS

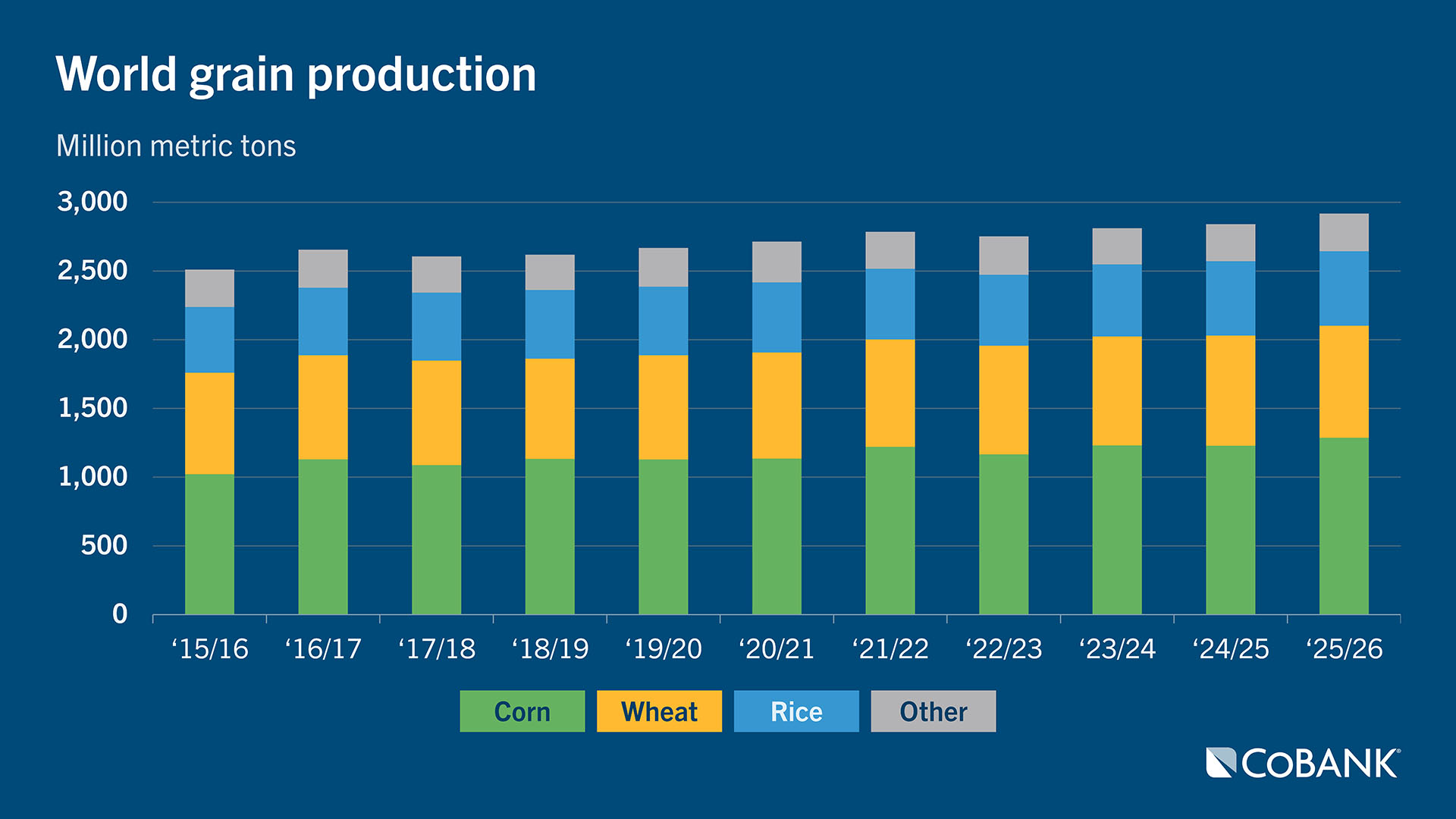

For oilseeds, a record soybean harvest in Brazil—paired with record oilseed production in countries like Kazakhstan that enjoy proximity to China—will erode U.S. soybean export competitiveness into China in 2026. World grain supplies are also ample with enlarged harvests in virtually every major exporting country for corn and wheat, which will compete with U.S. exports. Hope remains that China will start buying U.S. sorghum again, which would provide much-needed support to feed grain prices.

Source: USDA-FAS

There is an upside. Demand for U.S. grains and oilseeds will continue strengthening as low prices do the arduous work of stimulating usage. Mexico, the most important destination for U.S. corn, wheat and rice and the second-most important soybean destination, will continue to grow in importance. Demand for wheat and flour will continue its ascent in sub-Saharan Africa. The Middle East and Southeast Asia are increasingly turning to high-quality U.S. soybeans and soymeal to feed growing poultry flocks and livestock herds. A potential weakening of the U.S. dollar may give U.S. exports an additional tailwind.

Rising biofuel demand around the world further strengthens the demand story for grains and oilseeds. In the U.S., policy resolution on EPA’s renewable volume obligation and small refinery exemptions should bring greater clarity on blending rates, particularly for biomass-based diesel where EPA proposed significantly greater blending rates. Regulatory clarity will bring much-needed market certainty—and stimulate demand for fats and vegetable oils as feedstock for biofuel producers. Abroad, higher blending mandates for biomass-based diesel in Brazil and Indonesia will further tighten global vegoil supplies and improve crush margins for processors.

The soybean meal export market, though, will become increasingly competitive as oilseed crush capacity further expands in the U.S. and Brazil to produce vegoils for biofuel production. Regions like Southeast Asia, Latin America and the Middle East will be key battlegrounds between the U.S. and Brazil for soybean meal export market share.

Livestock end users will benefit from low feed costs through 2026 which will incentivize feed usage. Growth in feed demand, though, will be modest. The U.S. poultry flock will continue its steady recovery from losses to bird flu while the hog herd atrophies following a period of global oversupply. The beef cattle herd—the main driver of feed demand—will continue to struggle in its recovery barring a return of Mexican cattle imports. However, with low feed costs, feed usage per animal will likely continue expanding.

Grain and oilseed farmers will face hard choices for planting this spring. Although prevailing prices of nearly all crops are below the cost of production, soybeans have maintained their value relative to crops competing for acreage including corn, wheat, grain sorghum, cotton and rice. Current price ratios indicate soybeans stand to pull acres from all major crops. On the Plains, ample moisture may have caused some farmers to increase winter wheat seedings with plans to double-crop soybeans or grain sorghum following wheat harvest. High input costs may also discourage farmers from planting corn and switch to cheaper alternatives.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.