As a mission-based cooperative lender and member of the Farm Credit System, CoBank is committed to serving as a good corporate citizen. The bank maintains a variety of corporate social responsibility programs primarily focused on rural America and the vitality of rural communities and industries.

We deliver vital support for the U.S. rural economy, providing financial services to agribusinesses and rural power, water and communications providers in all 50 states. It's who we are and what we believe in. Join us.

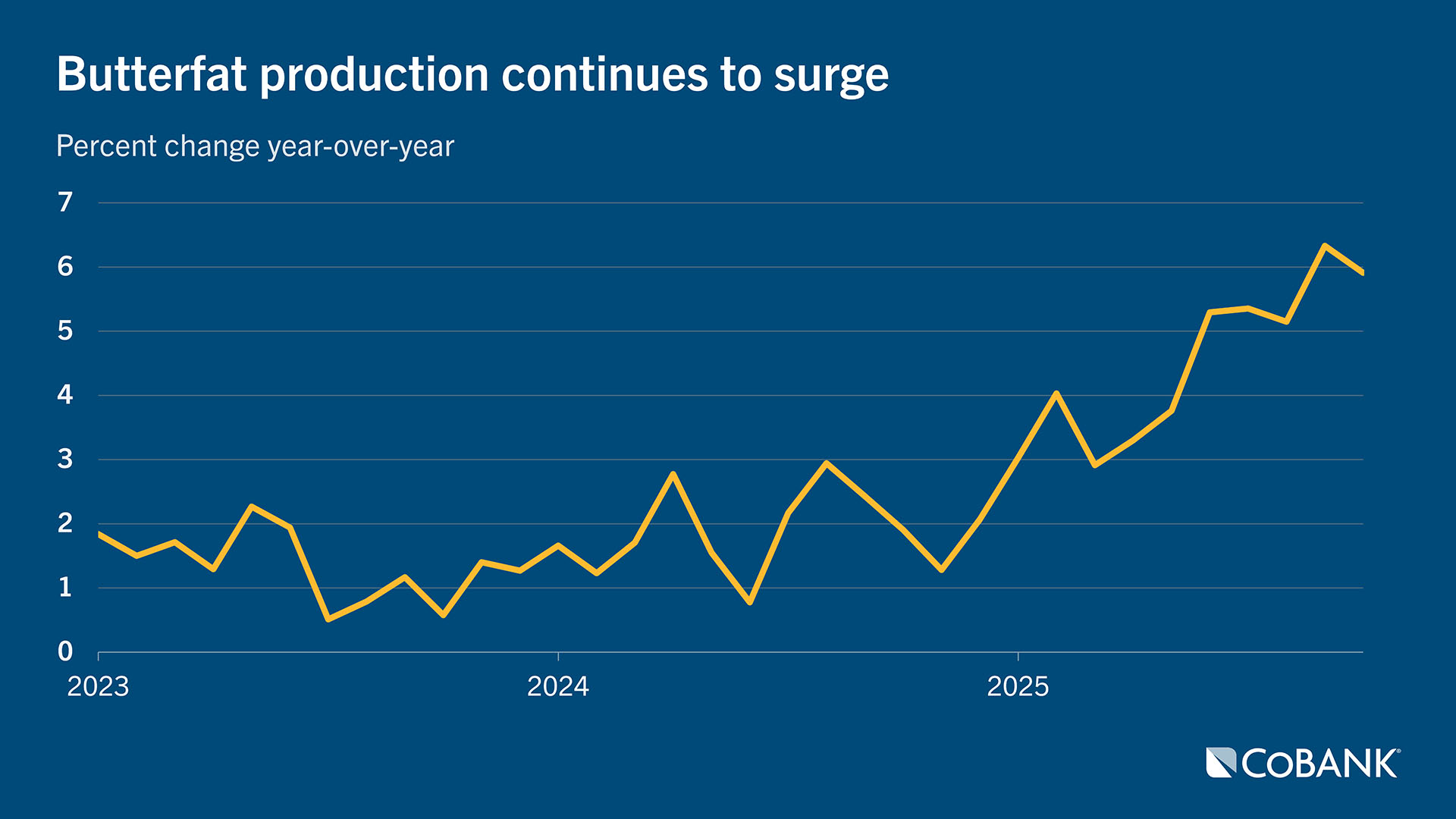

While demand for full-fat dairy products remains strong, butterfat has moved to an oversupply with 5% to 6% gains in the past five months.

With major investment in plants to make protein-based dairy products, milk protein is poised for a bull-market run.

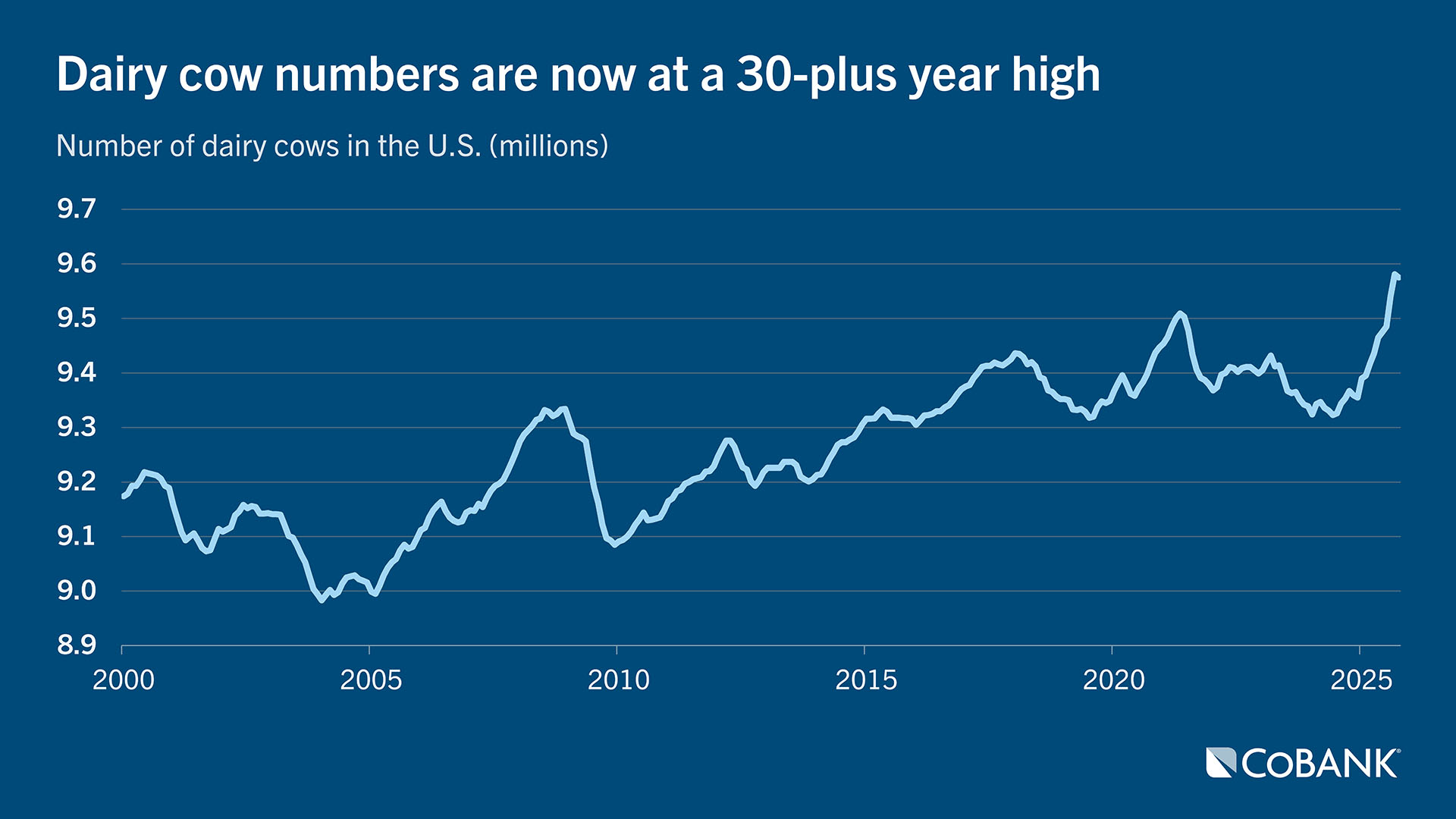

Strong demand for beef-on-dairy calves will continue to keep the U.S. dairy-cow herd at 30-year highs.

When given financial incentives, U.S. farmers are extremely talented at producing the product in demand. Dairy farmers are no exception. Over the past decade, butterfat led milk checks for eight of the 10 years. By 2021, the nation’s milk supply broke a seven-decade-old record for butterfat content at 3.95%. Inspired by milk check incentives, those records were shattered every year since, and this year butterfat will post another record close 4.3%. Keep in mind that butterfat levels were at 3.66% as recent as 2010.

Source: USDA-AMS and FMMO

While consumers continue to demand high butterfat products to this very day, dairy farmers are simply producing too much of a good thing and have created an oversupply situation as butterfat pounds have posted previously unfathomable 5% to 6.3% year-over-year gains in recent months.

Source: USDA-NASS and FMMO

As a result, dairy processors are awash in butterfat, and some have even put in caps on butterfat payment levels on farmgate milk in response to the situation. A year ago, this butterfat cap would not have been on anyone’s decision radar. These caps mirror some of the base excess plans from a recent era where some processors placed ceilings on the pounds of liquid milk shipped to their respective processing plants.

This year, oversupplies of butterfat are a discussion topic at every dairy meeting across the nation. However, there’s no such discussion about protein caps. In fact, protein markets are as strong as ever and could remain so for many years to come. Protein ranks as one of the must-have macronutrients among domestic and international consumers.

In addition, 23% of U.S. households are now using GLP-1 weight loss medications and those consumers have a stronger appetite for high protein foods to help maintain healthy muscle mass. Recent news about obesity drugs going mass-market and even being eligible for Medicare and Medicaid could put the protein trend in overdrive.

This all points to the market reality that protein will be the leading driver in milk checks in the coming years. This economic indicator is reinforced by the historic $11 billion in dairy plant investments. Cheese plants lead the way at $3.2 billion. Nearly every cheese plant now coming online brings an equally important strategy to capture protein value from the whey stream. Whey is no longer a byproduct.

Next in line is the $3 billion investment in fluid milk plants, many of which are making high-protein beverages and milk shakes from ultra-filtered milk. Unfortunately, these plants are spinning off more sweet cream that must find a market home, which adds to the butterfat surplus.

Rounding out the “big three” is $2.8 billion in dairy plant investment for yogurt and cultured dairy products. Anchoring that category is Greek yogurt, and to a lesser extent cottage cheese, both products that are rich in protein.

Overall, cheese and whey, fluid milk and yogurt plant investments cover just over 80% of the new and expanded dairy processing assets which stand as the leading testament for the value of dairy protein. On top of this dairy product outlook, four dairy products rank among the top 10 protein products for absolute unit growth in the past 52 weeks according to Circana and DMI data:

No. 2, dairy yogurt

No. 3, natural cheese

No. 6, cottage cheese

No. 10, dairy cream and creamers

Another reason to be bullish on protein is the fact that it is harder to produce on the dairy farm. While dairy farmers have feeding strategies and genetic tools to improve butterfat, the most economical improvement tool for protein is genetics, with few feeding strategies to significantly boost protein. Then there’s the fact that if we put full selection pressure in genetic programs on protein, we will improve butterfat at roughly an 80% rate as the two traits are highly correlated. That means protein growth will be a slow roll, and the protein-to-butterfat ratio may not improve over the 0.80 threshold, continuing to negatively impact cheese quality and production.

Source: USDA-NASS

Speaking of protein trends, the beef-on-dairy movement also shows no signs of slowing over the next three-year horizon. While there will be ebbs and flows in daily market values, the long-term trajectory indicates that the beef heifer and cow numbers are not close to entering a substantial rebuilding phase. On the flip side, U.S. dairy cow numbers have climbed by 228,000 head in the past year to reach 9.58 million head. Those numbers, now at 30-year highs, have grown in part to capture these record-high calf values.

Disclaimer: The information provided in this report is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. The information contained in this report has been compiled from what CoBank regards as reliable sources. However, CoBank does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will CoBank be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Stay ahead of the game in your field. Subscribe today.

Get CoBank's industry-leading Knowledge Exchange research reports delivered straight to your inbox as soon as they're released.

Have a comment or question about these reports?

Contact CoBank's Knowledge Exchange team to ask questions, engage with analysts or receive additional information.